Goldman Sachs expects Brent crude to reach $65 a barrel in the third quarter of 2021, although it could end the year lower, at $58 a barrel, according to Goldman Sachs analysts.

In a note, they also said they expected West Texas Intermediate to rally to $55.88 a barrel by the third quarter of next year, up from $51.38 a barrel in earlier forecasts, Business Insider reports.

“There is a growing likelihood that vaccines will become widely available starting next spring, helping support global growth and oil demand, especially jet,” the Goldman analysts said.

“Key to the resilience of spot prices, despite stalling inventory draws this summer, has been the steady rally in long-dated prices,” they added.

Earlier this year, the investment bank’s head of commodities Jeffrey Currie said that the short-term prospects of oil remained weak, but in 2021, prices would start to improve more markedly. He noted in July that if prices increased quickly, they would interfere with the market rebalancing by bringing more shale production back online.

Separately, Goldman analysts said back in July that demand for oil would likely recover to pre-crisis levels by 2022, spurred by a return to work for millions, a shift towards more private transport, and government support in the form of infrastructure spending.

In their latest note, the investment bank’s analysts said they expected oil demand to improve by 3.7 million bpd between January and August next year, while supply remains capped thanks to OPEC+’ continuing production cuts and a modest increase in non-OPEC supply.

Oil started this week with a gain, rising to the highest in five months on the back of positive economic news from China, a weak greenback, and plans by the UAE’s state oil company to reduce crude oil supplies by as much as 30 percent in October.

By Irina Slav for Oilprice.com (View Full Article Here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-09-01 10:38:002020-09-01 10:38:00Goldman Expects Oil To Reach $65 Next Year

Global oil demand is set to recover to near pre-covid-19 levels by the end of this year, Saudi Arabia’s energy minister Prince Abdulaziz said today prior to the OPEC+ Joint Ministerial Monitoring Committee meeting today, according to The National.

Specifically, Prince Abdulaziz expects that oil demand will recover to 97% of the levels pre-Covid.

That 97% is also the compliance rate that OPEC+ achieved in July, after promising to cut 9.7 million barrels per day off the group’s oil production levels.

Saudi Arabia has leaned hard on the members of the group that have not complied with the cuts to the same dutiful—and painful—level that Saudi Arabia has. The laggards of the group include Iraq and Nigeria, who have missed their quotas by large margins.

In response, Nigeria and Iraq—along with the other laggards Kazakhstan and Angola—have agreed to continue cut enough production to make up for ill compliance during the last couple of months.

“We should endeavor to put this temporary compensation regime behind us, by clearing all the past overproduction by the end of September,” Prince Abdulaziz said before the meeting.

But that would indeed be an ambitious undertaking for Nigeria and Iraq, who have had trouble complying to all OPEC agreements thus far, and who have not shared any specific plan to bring their oil production into compliance with the group’s agreement.

Regardless of the laggards’ poor showing, Prince Abdulaziz has noted that the oil market has shown signs of improvement with a drawdown in global inventories, a decline in floating storage, and a recovery in gasoline and diesel demand.

Oil prices were trading slightly down on Wednesday, even after the EIA reported crude oil and gasoline inventories draws for the week, and even after Prince Abdulaziz’s positive talking points.

By Julianne Geiger for Oilprice.com (View full article here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-08-20 10:06:222020-08-20 10:06:22Saudi Oil Minister: Oil Demand Could See A 97% Recovery By The End Of 2020

A crude oil inventory draw of 1.6 million barrels sent oil prices higher today, with the Energy Information Administration also reporting a fall in gasoline inventories and a modest build in distillate fuel inventories.

This compared with a draw of 4.5 million barrels for the previous week, the third weekly draw—and hefty—in a row.

A day earlier, the American Petroleum Institute cooled oil bulls’ optimism by estimating a gasoline inventory build of close to 5 million barrels for the week to August 14.

The EIA, for its part, estimated gasoline stockpiles had shed 3.3 million barrels last week, versus a modest decline of 700,000 barrels. Gasoline production last week fell, to 9.4 million bpd from 9.6 million bpd a week earlier.

Distillate fuel inventories rose by 200,000 barrels in the week to August 14, after a 2.3-million-barrel draw estimated for the previous week. Distillate fuel production averaged 4.7 million bpd, versus 4.8 million bpd for the previous week.

Refinery runs fell to 14.5 million bpd last week from 14.7 million bpd the week before.

Brent crude traded at $44.89 a barrel at the time of writing, with West Texas Intermediate at $42.44 a barrel in what is shaping up to be a mixed-results week. Oil started the week with a rise on the back of reports China was planning to ramp up oil imports from the United States but the budding rally ended soon amid doubts that the U.S. economy was recovering as quickly and consistently as it should be.

On top of that, OPEC+ is meeting today to discuss the progress of its production cut deal and future plans, adding a new angle of uncertainty. Even though no surprise news is expected to come out of this meeting it could tell traders how the deal is going and whether internal agreement remains robust.

OPEC+ boasted record compliance in July, at a combined 94-97 percent, according to different surveys.

By Irina Slav for Oilprice.com (View full article here)

Bank of America expects oil prices to recover to $60 a barrel for Brent crude in the first half of next year thanks to shrinking global inventories and prices improving faster than previously expected.

“Back in June, we upped our oil price forecasts by $5 per barrel (/bbl) and argued that Brent would average $43/bbl in 2020 and $50/bbl in 2021,” Bank of America’s analysts said as quoted by Trade Arabia.

However, since then, oil futures have been rising faster than expected even though spot prices remained range-bound, the bank noted. Because of this and because it expects an oil market deficit of 4.9 million bpd for the second half of this year and another of 1.7 million bpd next year, BofA expects prices to shoot up.

The bank’s analysts noted the slump in drilling rigs, notably in the U.S. shale patch, and the OPEC+ oil production cuts as some of the main factors that would push the oil market into a deficit and prop up prices.

However, the demand side remains a downward pressure for prices. The IEA and OPEC were the latest to sound a cautious note in their respective monthly reports. The IEA said it expected oil demand this year to be down 8.1 million bpd from last year, while OPEC estimated a demand loss of 9.1 million bpd this year.

With so much demand lost, the news that supply was on the rise in July did not sit well with oil traders. According to the IEA, supply rose 2.5 million bpd last month as Saudi Arabia relinquished its voluntary additional cuts of 1 million bpd and as the UAE fell short of its production quota. U.S. output also began to rise in July, casting a shadow over expectations of supply tightening.

According to ANZ, oil demand currently stands at 88 million bpd. That is up 8 million bpd on April but still 13 million bpd below demand levels from August 2019.

By Irina Slav for Oilprice.com (View Full Article Here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-08-17 09:59:582020-08-17 09:59:58Bank Of America: Brent Will Recover To $60 In H1 2021

The market is gradually beginning to give credence to something I’ve been discussing in past OilPrice articles for a long time now. In a June, 2020 article entitled, Underinvestment Could Send Oil Prices Soaring, I argued how the retrenchment and lack of capital investment the industry has seen the past five-years would lead to shortages of crude eventually. The huge volume of Saudi overproduction exacerbated the equal largess in American shale for the past couple of years, and led to a glut of crude globally.

EIA-WPSR The blue line shows weekly storage numbers beginning to edge back into the five-year range.

We are now starting to work off this glut as noted in the weekly EIA petroleum status report above, and the day of reckoning I forecast in June is just around the corner, a few months hence at most. Even the news in July that OPEC+ would start restoring as much as two-million BOPD through the end of the year, failed to quiet the unease beginning to take hold in the market. News like that would have sent prices into the cellar in May, having left the current contracts above $41 for WTI and near $45 for Brent.

Take the two bullets below to the bank.

Supplies of crude oil are going to drop, just as demand is on the increase.

Oil prices are going to continue advancing higher.

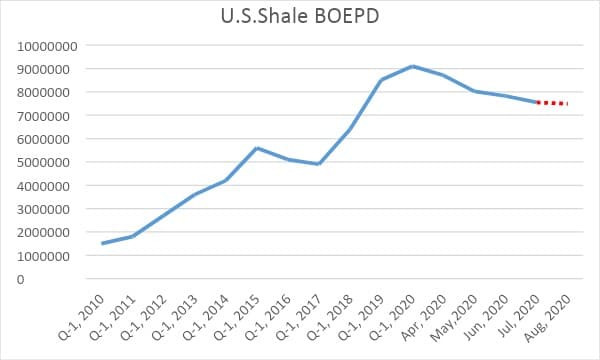

In the rest of this article we will give a forecast of where we see end-of-year U.S. daily production and the impact that will have on prices for the two most closely followed benchmarks, WTI, and Brent.

The Permian

Focusing on the Permian as it alone accounts for over half of U.S. daily shale production, let’s note the slope of the decline that began in March, and accelerated in April.

Obviously, the dramatic drop in production from April to May was primarily a product of the shut-in campaign producers waged to try and lever prices higher. A campaign we’d have to call a success, as prices have risen from $12.34 to over $42 since April, 28th.

June’s 914 will probably show a moderation or even an increase as producers started to bring production back mid-month in June, and continued on into July as prices ramped. I think that will probably be it and production will start a sharp decline through the end of the year. I stick to my prediction of a shift in mentality from, “I can get all of the oil I want all of the time,” to, “Where is my next load of oil coming from.” That’s my feeling for the start of Q-1, 2021.

Key Bullish indicators for oil prices

Drilling– no question, the continued decline in drilling in the USA has sealed the fate for shale, which is bullish factor number 1 for oil prices. Shale production has peaked and we will never again see shale production of over 9 mm BOPD. For the week ending Aug-7th the Baker Hughes rig count dropped slightly versus the week prior, continuing a five-month, largely uninterrupted trend down.

What does this profound decline in drilling portend? From January to now we’ve lost ~550 rigs. At an average of 800 BOPD per rig that’s 440K of new production we haven’t seen. Legacy decline amounts to about 300K BOPD through May. Those two numbers together come to roughly 750K BOPD. With only 246 rigs adding to new production there is a gap of ~500K BOPD from drilling activity YoY alone. The problem of the high legacy decline will only accelerate as this year closes out, and 2021 dawns.

Russia– The outlier in the OPEC+ duopoly reported that its production had fallen 16% YoY. This suggests that it has been following its commitment in the current OPEC+ production cut. Cuts that are now being gradually restored. There had been a good bit of rumbling about whether Russia was sticking to this agreement. News that is has is bullish for the oil market.

Libya – Years of political strife have wrought a toll on this OPEC producer. OPEC’s Monthly Production report paints a gloomy picture with their production dropping from 1.1 mm BOPD last fall to 82K as of June. A lot of this loss is probably permanent as equipment is not being maintained, reservoirs are being damaged from water influx, etc.

Venezuela – Oil production in this nearly-failed state has fallen to around 375K BOPD as of the end of June. In the last 20 years this country’s oil production has dropped from ~3.5 mm BOPD to present levels. This situation is unlikely to resolve itself favorably in the upward direction anytime soon as the very last rig still drilling in the Orinoco has been laid down, as per this Forbes Article.

OPEC+ – Sensing that their gambit to raise prices has been at least partially successful, has begun to restore production. This metric while not bullish in and of itself, is notable in the manner that this shut-in production will come back. With an eye toward gradually increasing oil demand for the rest of this year, OPEC+ will gradually add back about 2-mm BOPD through year-end. With ~5-months left to go this amounts to about 400K BOPD per month. This is helping to sustain the oil price rise as demand growth will easily absorb this amount.

The Economy – The bullishness that overcame the market in June, and began to dissipate in July put a top on oil prices. Inventory builds that occurred then sent ambiguous signals into the market. As we go into August, what’s becoming increasingly clear is we are adapting to this new reality faster than anyone thought possible. While the V shaped recovery is off the menu, we are recovering in terms of employment and overall business activity. Last the Wall Street Journal reported that 1.5 mm new jobs were added in July, dropping the unemployment rate to 10.6% of the working population.

Key OFS – Companies are raising hopes for the future, as noted by Halliburton’s CEO in their quarterly conference call, “a gradual recovery was underway.” A sentiment that was present in a number of conference calls for the second quarter.

Covid-19 – The good news here tends to be lost in the higher infection rate noise of Q-2. The real story is that the mortality rate is much less than initially thought, and the really good news is that relief-real relief is in sight. I am talking of course about vaccine trials, as noted in a recent Wall Street Journal article. The news here is unreservedly bullish.

Stimulus – The government basically fulfilled its function of stepping in in a number of ways to provide the trillions of dollars of stimulus and liquidity the market has demanded earlier this year. In my opinion more of this is needed, and I hope our political leaders can come together to provide it. There’s a narrative about the amount of new debt that’s been created. This narrative loses sight of the depth of decline small business has seen compared to bigger companies. A new PPP program is absolutely needed to avoid a severe recession. There is no doubt in my mind, the government will again shore up the economy with a program similar to the one prior. President Trump’s recent Executive Orders are a good start. More will come.

The Key Bearish indicator

China– Demand from China has been one of the things that’s helped to take excess oil off the market. Unofficial estimates made in a Reuters article suggest that China was responsible for about 3-mm BOPD of purchases in excess of their internal demand. Doing this while oil was really cheap to keep their costs low. Now that oil has doubled from March lows, there is a narrative these purchases may slow. The market can certainly absorb some oil in addition to what OPEC+ will be restoring, but how much is the question. Associated with that is the amount of floating oil stored in ports on tankers. Another recent Reuters article estimated that there were as many as 120 mm bbls waiting to be offloaded in Chinese ports.

Outliers

What could change the dynamic one way or the other is the lack of belligerence in the world currently. That could change at any time, and is impossible to predict. There is no war premium in oil currently.

Iran which people have been saying was going to implode at any moment for the past year, still defies sanctions on its nuclear industry. My view is that while the world has been occupied for most of this year with Covid-19, as this begins to abate there will be renewed pressure on Iran. A war premium would add $50 a bbl to the oil price over-night.

In a move to re-nationalize its oil reserves, Mexico seems to be moving to drive out foreign investment in coming years, reversing a previous trend toward welcoming foreign capital. This as their production has entered a gradual production decline from 2.3 mm BOPD to about 1.75 mm BOPD during the last five years.

Oil companies are becoming leery of deploying capital in marginal areas, as noted by the huge asset valuation write-downs taken by all of the Super Major oil companies in the first half of this year. Any notion that their capital is going to be subjected to an eventual heavier tax regime, or outright nationalization, will send them into hibernation.

Your takeaway

Overall, the case for oil supplies and production rates continuing to diminish and for prices to continue to rise, is stronger than the inverse scenario. We expect year-end U.S. domestic shale production to be in the neighborhood of 5-mm BOPD. This represents a YoY decline of about 45%. This stark view is not widely held by the market, notably with the EIA-STEO forecasting the decline to be only about 2-mm BOPD. That’s the problem with forecasting- you never have enough data.

Here’s what we know. In January of 2020 with 805 rigs running U.S. shale production peaked at 9.3 mm BOPD. A moderate decline rate of 50% (annual shale decline rates vary from 30% for great, Tier I acreage wells, to as high as 70% YoY for lower tiers or poorly completed wells.), for legacy decline from the first of the year would see production halved.

If 2020 averages 435 rigs per day, that’s ~350K BOPD new production from drilling for the year. In that scenario we add that new oil to what’s left after legacy decline, ~4.6 mm BOPD, and we get ~5-mm BOPD.

Numbers don’t lie. This is admittedly simple math for an incredibly complex actual-almost incalculable calculation, but if I am even close to being right, and storage truly does get worked off around the world…get ready for $100 oil.

By David Messler for Oilprice.com (View full Article here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-08-11 10:12:242020-08-11 10:12:24Here’s How Oil Could Skyrocket By 138%

Libya’s port blockade is set to keep the North African country’s oil off the market until at least the fourth quarter of 2020, which, as devastating as it will be for Libyan oil revenues, could help reduce the expected global production glut by 65 percent, Rystad Energy said on Friday.

Currently, oil production in Libya is around 100,000 barrels per day (bpd). This figure is dramatically down from 1.2 million bpd at the start of the year, just before paramilitary formations affiliated with the Libyan National Army (LNA) of eastern Libyan strongman General Khalifa Haftar occupied Libya’s oil export terminals and oilfields.

With Libya’s conflict escalating, the country’s crude oil exports are expected to be just 1.2 million barrels in August, a 40-percent plunge from July, Bloomberg reported earlier this week, citing an initial loading program it has seen.

With no immediate return of Libyan oil on the market, the expected global production surplus later this year could be just 58.6 million barrels or about one-third of Rystad Energy’s previous forecast.

Even if Libya resumes most of its production soon, in the most optimistic scenario by Rystad, Libya’s 2020 exit production rate will be between 700,000 bpd and 800,000 bpd. The country, however, will need another up to four months to ramp the production up to 1 million bpd. Related: Venezuela’s Rig Count Officially Falls To Zero

NOC’s chairman Mustafa Sanalla has recently said that “The illegal oil blockade has had disastrous effects on our national economy and damaged the living standards of Libyans. Our reservoirs are suffering permanent damage, and stagnant fluids are corroding our pipelines, which will cost us huge amounts to repair.”

According to Bjornar Tonhaugen, Rystad Energy’s Head of Oil Markets, Libya will inadvertently help reduce the production surplus on the global oil market.

“Our latest global liquids balances report still suggests there will be a shift towards a surplus from August and for the ensuing three months, but it is less precarious than previously estimated and developments in Libya have a lot to do with this revision,” Tonhaugen said.

By Charles Kennedy for Oilprice.com (View full article here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-08-10 14:16:442020-08-10 14:16:44Libya’s Oil Blockade Will Help Clear The Global Supply Glut

The world’s biggest oil-producing and oil-exporting company, state oil giant Saudi Aramco, is optimistic about the pace of oil demand recovery in Asia, chief executive Amin Nasser said on Sunday, helping oil prices rise on Monday.

“We are seeing a partial recovery in the energy market as countries around the world take steps to ease restrictions and reboot their economies,” Nasser said in a statement following Aramco’s Q2 report released over the weekend.

Demand for crude oil in Asia has almost returned to the levels from before the pandemic, Bloomberg quoted Nasser as saying.

At the end of June, Nasser said that the worst in the oil market was over, and noted that he was “very optimistic” for the second half of this year.

In June, global oil demand is somewhere around 90 million barrels per day (bpd), up from 75-80 million bpd in April, Nasser told IHS Markit Vice Chairman Daniel Yergin in an interview for CERAWeek Conversations two months ago.

Saudi Aramco’s comments on Sunday about the demand recovery were one of the key reasons for oil prices rising early on Monday, according to analysts.

In another sign of optimism about demand, data from global flight tracking service Flightradar24 showed on Saturday that on Friday, August 7, there were more than 70,000 commercial flights globally for the first time since March 20. Yet, the number of commercial flights was still down 43.6 percent compared to the same Friday in August 2019.

After a drop on Friday, oil prices rose early on Monday, with the U.S. benchmark up more than 2 percent as of 9:47 a.m. EDT. WTI Crude rallied 2.28 percent at $42.21 and Brent Crude was trading above $45—at $45.20, up by 1.76 percent on the day.

By Tsvetana Paraskova for Oilprice.com (View full article here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-08-10 13:42:502020-08-10 13:42:50Saudi Aramco: Asian Oil Demand Recovery Almost At Pre-Crisis Levels

Oil prices hit a four-month high on Tuesday as the promise of major stimulus packages in the EU and the U.S. counter-balanced an increase in COVID cases.

Chart of the Week

– U.S. liquid fuels consumption is expected to continue to rise in the second half of 2020, but will remain below pre-pandemic levels until August 2021, according to a new forecast from the EIA.

– For the full year, the EIA sees gasoline demand averaging 8.3 mb/d, down 1 mb/d year-on-year, or a 10 percent decrease.

– Still, the EIA’s forecast is at the optimistic end of most predictions. For instance, the agency sees jet fuel demand being down only 12 percent next year. Other analysts see long-lasting scars to aviation.

Market Movers

– Marathon Petroleum’s (NYSE: MPC) Tesoro High Plains pipeline was ordered to shut down for the first time in 67 years after the U.S Department of Interior’s Bureau of Indian Affairs determined the pipeline trespassed on Native American land. The pipeline moves Bakken oil through North Dakota.

– Halliburton (NYSE: HAL)jumped more than 8 percent after reporting second-quarter results that beat expectations. Halliburton “inked simply outstanding results vs. expectations… [as] structural cost cuts are clearly bearing fruit,” Tudor Pickering Holt analysts say. Halliburton took a $2.1 billion impairment.

– Total (NYSE: TOT) secured financing for its $15 billion Mozambique LNG project.

Tuesday, July 21, 2020

Oil prices rose sharply on Tuesday. Despite bad coronavirus news in the U.S., which could weaken demand, there are high hopes for economic stimulus. The European Union agreed to a historic stimulus, and the U.S. Congress appears intent on passing yet another trillion-dollar economic package. Crude prices hit four-month highs on Tuesday.

Chevron buys Noble for $5 billion.Chevron (NYSE: CVX) announced the purchase of Noble Energy (NASDAQ: NBL) for $5 billion, an all-stock deal worth $13 billion when including debt. The move adds U.S. shale assets in the DJ Basin and, crucially, a large presence in the Eastern Mediterranean. The deal was the first major M&A move since the onset of the pandemic. Related: Newcomer Brazil Steals Market Share In Key Asian Oil Market

Australian LNG hit by impairments. Australia’s LNG sector has been hit hard by multiple impairments from domestic and international gas companies. Woodside Petroleum (ASX: WPL) recorded a $4.37 billion impairment, and Royal Dutch Shell’s (NYSE: RDS.A) massive $15-$22 billion write-down was led by Australian LNG. “Realized prices have dropped dramatically due to global oil oversupply and demand destruction from the pandemic,” a Woodside executive said on an investor call.

Natural gas prices fall. Natural gas prices fell sharply on Monday after data showed another dip in U.S. LNG exports.

Fewer canceled U.S. LNG cargoes for September. The volume of U.S. LNG cargoes canceled by buyers for September slowed compared to preceding months. The exact number is unclear, but Reuters reports that somewhere between 15 and 26 cargoes have been canceled for September delivery, a smaller number than the 40 to 45 reported for July and August. Cheniere Energy (NYSE: LNG) (NYSEAMERICAN: CQP) has the most canceled cargoes.

Brazil boosts oil exports to Asia. Brazil’s oil exports to Asia averaged 1.07 mb/d in the first six months of 2020, a 30 percent year-on-year increase.

Saudi Arabia wants more than $40. The OPEC+ deal has succeeded in tightening up the market and boosting oil past $40, but Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, has highlighted that although OPEC itself does not have a price target, current prices are not sustainable for the industry, leading to potential insecurity of supply in the long term.

EV investor craze continues.Tesla (NASDAQ: TSLA) saw its market cap surge past $300 billion and investors are piling into other EV makers. Tesla’s shares have more than tripled this year. The market value of Nikola Corp. (NASDAQ: NKLA), an electric truck startup, past Ford (NYSE: F) last month, although the company’s stock has since retreated. The trend shows that investors increasingly believe that EV era will arrive faster than previously thought. Carmakers are rushing to capture a slice of the future, with GM (NYSE: GM) recently announcing that it will develop 20 new EV models by 2023. Including hybrids, the global auto industry will add 350 new models in the next few years.

North Dakota oil plunges 30 percent. North Dakota’s oil production plunged 30 percent from April to May, collapsing to just 850,000 bpd. It was the worst-ever monthly decline. “The second quarter of 2020 was a five-alarm fire for North Dakota’s oil and gas industry,” state Mineral Resources Director Lynn Helms said on a conference call. However, shut-in production is coming back online. Meanwhile, the potential closure of the Dakota Access pipeline raises tough questions about the region’s future.Related: Can Saudi Arabia Extend The OPEC Deal Until 2022?

EU to US: Stop threatening sanctions. The EU warned the Trump administration to stop threatening European companies with sanctions over the Nord Stream 2 pipeline.

EU near green stimulus. After days of negotiating, the European Union has agreed to a major stimulus package, including more than half a trillion euros dedicated to green stimulus.

Total and Exxon idle workers in Papua New Guinea.Total (NYSE: TOT) and ExxonMobil (NYSE: XOM) have idled workers at the Papua New Guinea LNG expansion project due to the pandemic. The project had previously faced delays due to negotiations with the government.

New Mexico releases methane rule. New Mexico unveiled a draft methane regulation, with a target of capturing 98 percent of natural gas by 2026. The effort to cut flaring comes just as a federal judge shot down the Trump administration’s efforts to rescind federal methane regulations. Meanwhile, the World Bank published a report that found that gas flaring worldwide increased by 3 percent last year to the highest level in more than a decade – 23 percent of the increase came from the U.S.

Halliburton a “Strong Buy.” Raymond James issues a Strong Buy rating for Halliburton (NYSE: HAL) after the oilfield services giant vastly exceeded expectations in its second-quarter earnings. “Halliburton’s 2Q20 was extremely strong as the company’s quick cost actions limited decremental margins in the face of the extreme decline inactivity,” the bank said.

By Josh Owens for Oilprice.com (view full article here)

Saudi Arabia could use this summer record amounts of crude oil for producing electricity as more Saudis would stay at home rather than travel on vacation abroad because of the pandemic, according to Bloomberg estimates of analysts.

Saudi Arabia burns crude oil for power generation and this summer it could be on track to burn record volumes of crude to keep air conditioning on while temperatures outside could reach 120 degrees Fahrenheit.

The burning of more oil is a setback from earlier Saudi plans to reduce its reliance on crude for electricity generation. Saudi Arabia also has less natural gas to use for power generation this summer because the ongoing OPEC+ oil production cuts affect the associated natural gas production at its oil fields.

The Saudi choice for power generation this summer is either importing more natural gas or burning more crude oil, Carole Nakhle, chief executive officer at London-based consulting firm Crystol Energy, told Bloomberg.

“The second option is more likely and easier since the region has been doing this for years and decades and there is plenty of oil around today,” Nakhle said.

The higher crude-for-power-generation will absorb the extra crude oil production from Saudi Arabia after the OPEC+ cuts are eased from August 1, Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, said earlier this month.

Despite the higher production resulting from the eased cuts, the world’s largest oil exporter said last week that it would keep its crude oil exports in August at the levels from July.

“I can tell you that in the Kingdom Saudi Arabia, due to the increase in demand from utilities and other sectors, as lockdowns ease, we estimate approximately 500,000 barrels per day of extra demand in August. So, despite a higher production target in August, there will be no change in our exports,” Prince Abdulaziz bin Salman said last week at the Joint Ministerial Monitoring Committee (JMMC) meeting.

By Tsvetana Paraskova for Oilprice.com (view full article here)

https://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.png00Deane Brunerhttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngDeane Bruner2020-07-22 11:36:162020-07-22 11:40:29Saudi Arabia Set To Burn Record Crude Oil Volumes For Electricity

Shale gas, natural gas produced by hydraulic fracturing or fracking, has positively changed electricity production and the environment in the United States. Shale gas provides reliable, scalable electricity generation and is the dominate fuel used in the United States.

Recently greenhouse gas emission levels have declined in the U.S., and the primary reason is the switch from coal to natural gas in the power generation industry. It has the potential to change global energy markets and lower global greenhouse gas emissions.

https://www.apiresources.net/wp-content/uploads/2018/06/MotleyFool-TMOT-aa94c23b-106-fracking_large.jpg401534API Resourceshttps://www.apiresources.net/wp-content/uploads/2020/07/api-resources-logo-v2.pngAPI Resources2018-06-19 11:09:362018-06-19 11:09:36Natural gas – the miracle fuel